Medical insurance in the United States is one of the most important financial tools for protecting yourself and your family from expensive healthcare costs. Medical treatment in the USA is among the most expensive in the world, and even a short hospital stay can cost thousands of dollars. Without health insurance, patients may have to pay the full cost of doctor visits, surgeries, emergency care, prescription drugs, and hospital bills out of pocket. Choosing the right medical insurance plan helps reduce these expenses while providing access to quality healthcare services. Whether you are an individual, a family, a student, or a senior citizen, understanding how medical insurance works can help you make an informed decision and avoid unexpected medical costs.

What is Medical Insurance?

Medical insurance, also known as health insurance, is a contract between you and an insurance company. In exchange for a monthly premium, the insurer helps pay for covered healthcare services such as doctor visits, hospital stays, surgeries, prescription medications, preventive care, and emergency treatment. Depending on the policy, you may still pay deductibles, copayments, or coinsurance, but your overall healthcare expenses are significantly reduced.

Why Medical Insurance is Important in the USA

Healthcare costs in the United States continue to increase every year. A simple emergency room visit can cost hundreds or even thousands of dollars, while major surgeries may exceed tens of thousands of dollars. Medical insurance provides financial protection by covering a large portion of these expenses. It also gives policyholders access to preventive healthcare services, helping detect illnesses early before they become serious and expensive to treat. Having insurance also offers peace of mind because you know you can receive medical care when needed without worrying about overwhelming bills.

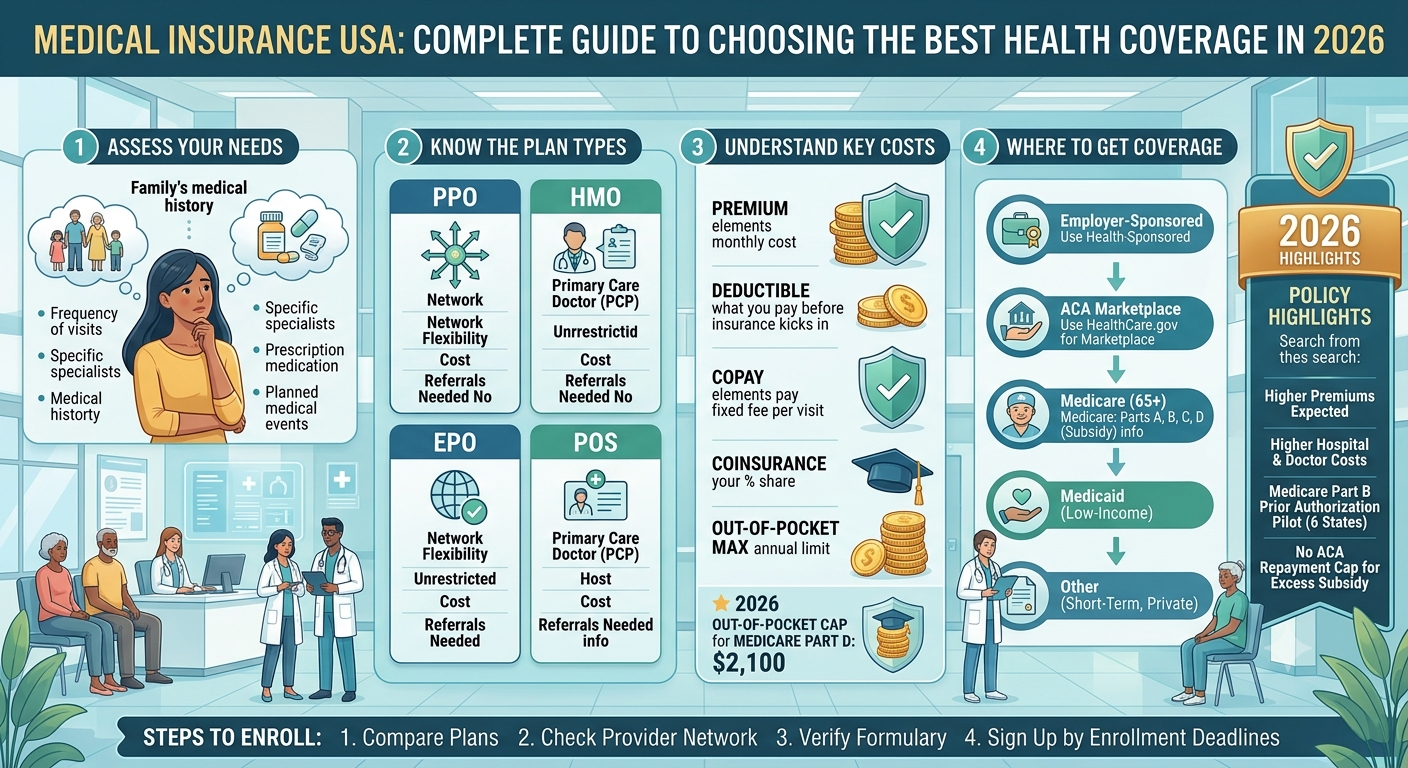

Types of Medical Insurance Plans in the USA

Health Maintenance Organization (HMO)

HMO plans usually have lower monthly premiums and require members to use doctors and hospitals within a specific network. Patients generally need a referral from their primary care physician before visiting specialists.

Preferred Provider Organization (PPO)

PPO plans offer greater flexibility by allowing patients to visit both in-network and out-of-network providers. Although premiums are usually higher than HMO plans, members enjoy greater freedom when choosing healthcare providers.

Exclusive Provider Organization (EPO)

An EPO combines some features of HMOs and PPOs. Members must generally use network providers but usually do not need referrals to see specialists.

Point of Service (POS)

POS plans require members to choose a primary care physician while allowing some out-of-network care at a higher cost.

High Deductible Health Plan (HDHP)

These plans have lower monthly premiums but higher deductibles. They are often paired with a Health Savings Account (HSA), allowing individuals to save money tax-free for qualified medical expenses.

What Does Medical Insurance Cover?

Most comprehensive medical insurance plans include a wide range of healthcare services. Coverage often includes doctor consultations, preventive care, annual health checkups, vaccinations, laboratory tests, X-rays, MRI scans, CT scans, emergency room visits, hospitalization, surgeries, intensive care, maternity care, mental health treatment, rehabilitation services, prescription medications, ambulance services, and preventive screenings. Some plans also include wellness programs, telemedicine services, and chronic disease management.

Common Medical Expenses Covered

Medical insurance typically helps pay for primary care physician visits, specialist consultations, emergency room treatment, ambulance transportation, hospital admission, intensive care unit services, surgical procedures, diagnostic imaging, laboratory testing, prescription drugs, outpatient treatment, physical therapy, preventive screenings, vaccinations, maternity care, pediatric services, mental health counseling, and rehabilitation programs.

Understanding Health Insurance Costs

Choosing the right medical insurance requires understanding several important cost factors.

Premium

A premium is the monthly amount you pay to keep your insurance policy active.

Deductible

The deductible is the amount you pay for covered healthcare services before your insurance company begins sharing costs.

Copayment

A copayment is a fixed amount you pay for specific services such as doctor visits or prescription medications.

Coinsurance

Coinsurance is the percentage of healthcare costs you pay after meeting your deductible. The insurance company pays the remaining percentage.

Out-of-Pocket Maximum

This is the highest amount you will pay for covered healthcare services during a policy year. Once this limit is reached, the insurance company pays 100% of covered medical expenses.

Best Medical Insurance Companies in the USA

Several leading insurance companies provide comprehensive health coverage across the United States.

UnitedHealthcare is one of the largest insurers, offering extensive provider networks, wellness programs, and comprehensive medical coverage.

Blue Cross Blue Shield provides nationwide coverage through independent companies and is widely accepted by hospitals and healthcare providers.

Kaiser Permanente combines health insurance with its own hospitals and healthcare facilities, providing coordinated medical care.

Aetna offers employer-sponsored, individual, and Medicare plans with access to a large network of healthcare professionals.

Cigna provides international coverage options, comprehensive medical plans, wellness services, and telehealth benefits.

Humana is especially popular for Medicare Advantage plans while also offering individual and family health insurance.

Oscar Health focuses on technology-driven healthcare with virtual doctor visits, digital tools, and personalized member support.

How to Choose the Best Medical Insurance Plan

Start by evaluating your healthcare needs. Consider how often you visit doctors, whether you take regular medications, and if you have any chronic health conditions. Compare monthly premiums, deductibles, copayments, and out-of-pocket maximums. Review the provider network to ensure your preferred doctors and hospitals are included. Carefully read policy exclusions, waiting periods, prescription drug coverage, preventive care benefits, and customer reviews before making your final decision.

Benefits of Having Medical Insurance

Medical insurance offers financial protection from unexpected healthcare costs while providing access to preventive services, specialist care, hospital treatment, emergency services, and prescription medications. Insured individuals are more likely to receive regular health screenings, vaccinations, and early treatment, leading to better long-term health outcomes. Comprehensive insurance also reduces financial stress by minimizing large medical bills after accidents or illnesses.

Tips for Saving Money on Medical Insurance

Compare plans from multiple insurance providers before enrolling. Choose in-network hospitals and physicians whenever possible to reduce healthcare costs. Use preventive care services because many are covered without additional charges. Consider an HSA if you enroll in a high deductible health plan. Review your insurance policy annually to ensure it continues to meet your healthcare needs and budget.

Common Mistakes to Avoid

Many people choose the cheapest plan without considering deductibles or network restrictions. Others fail to check prescription drug coverage or ignore policy exclusions. Some applicants underestimate their healthcare needs and purchase insufficient coverage, while others forget to verify whether their preferred hospitals participate in the insurer’s network. Reading the policy carefully before enrollment helps avoid these costly mistakes.

Frequently Asked Questions

Is medical insurance mandatory in the USA?

Federal law no longer requires most individuals to maintain health insurance, although some states have their own insurance requirements.

What is the best medical insurance company?

The best insurer depends on your location, healthcare needs, budget, provider network, and preferred hospitals. Companies like UnitedHealthcare, Blue Cross Blue Shield, Kaiser Permanente, Aetna, Cigna, Humana, and Oscar Health are among the most recognized providers.

Does medical insurance cover emergency hospital visits?

Most comprehensive health insurance plans cover emergency room treatment, hospitalization, ambulance services, and emergency surgeries according to the policy terms.

Can I buy medical insurance without an employer?

Yes. Individuals can purchase health insurance directly through private insurance companies or government health insurance marketplaces if eligible.

Does health insurance cover prescription drugs?

Many medical insurance plans include prescription drug benefits, although coverage varies depending on the plan and medication formulary.

Conclusion

Medical insurance in the USA is essential for protecting individuals and families against rising healthcare costs. A quality insurance plan covers hospital bills, emergency treatment, surgeries, doctor visits, prescription medications, preventive care, and many other healthcare services. When selecting a policy, compare premiums, deductibles, provider networks, coverage limits, and customer service to find the best value for your needs. Investing in comprehensive medical insurance today can provide financial security, better healthcare access, and peace of mind for years to come.

Related posts:

Best Hospitals in the USA 2025: A Complete Guide to America’s Top Medical Institutions

Best Hospitals in the USA 2025: A Complete Guide to America’s Top Medical Institutions

Best Organ Transplant Hospitals in the USA (2025): Where Life Gets a Second Chance

Best Organ Transplant Hospitals in the USA (2025): Where Life Gets a Second Chance

Best Hospital in Germany

Best Hospital in Germany

Health Insurance for Hospital Bills: A Complete Guide

Health Insurance for Hospital Bills: A Complete Guide

Fertility Hospital Near Me: Complete Guide to Choosing the Best IVF & Fertility Clinics

Fertility Hospital Near Me: Complete Guide to Choosing the Best IVF & Fertility Clinics

Best Private Hospital in Los Angeles: A Complete Guide

Best Private Hospital in Los Angeles: A Complete Guide

Cardiac Bypass Surgery in International Hospitals: Cost, Best Countries, and Patient Guide

Cardiac Bypass Surgery in International Hospitals: Cost, Best Countries, and Patient Guide

Best Hospital in Malaysia: Top International Healthcare Guide

Best Hospital in Malaysia: Top International Healthcare Guide

Top Fertility Clinics in America: Leading Centers for Advanced Reproductive Care

Top Fertility Clinics in America: Leading Centers for Advanced Reproductive Care

Best IVF Hospital in USA: Leading Centers for Advanced Fertility Treatment

Best IVF Hospital in USA: Leading Centers for Advanced Fertility Treatment