Hospital indemnity insurance is a supplemental insurance policy designed to help cover out-of-pocket expenses associated with hospitalization. While traditional health insurance pays for many medical services, policyholders are often responsible for deductibles, copayments, coinsurance, and other costs that can add up quickly during a hospital stay. Hospital indemnity insurance provides cash benefits that can be used for any purpose, giving individuals and families additional financial protection during medical emergencies.

Whether you have employer-sponsored health insurance, a private health plan, Medicare, or another type of medical coverage, hospital indemnity insurance can help reduce the financial burden of unexpected hospital bills.

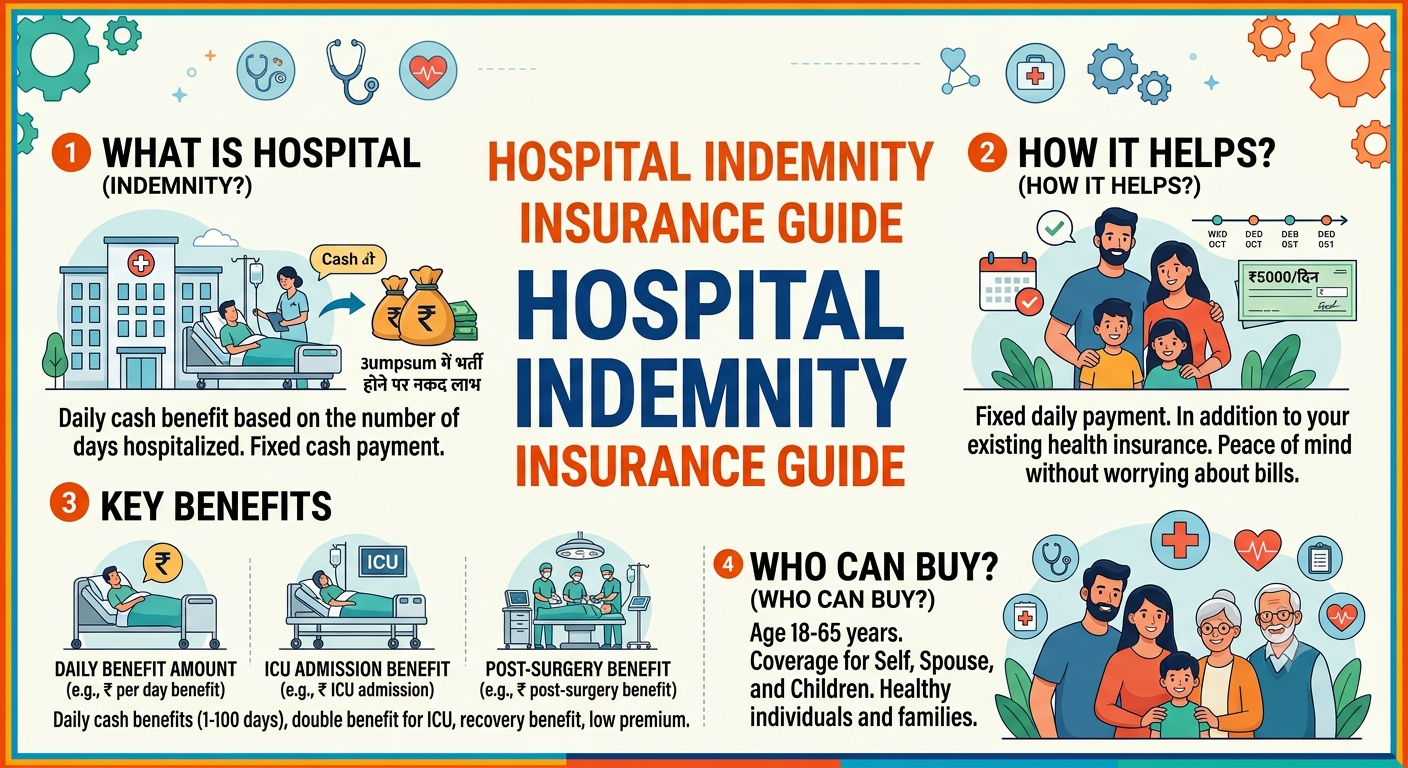

What is Hospital Indemnity Insurance?

Hospital indemnity insurance is a supplemental health insurance policy that pays a fixed cash benefit when you are hospitalized for a covered illness, injury, or medical procedure. Unlike traditional health insurance, the payment is made directly to the policyholder rather than the hospital or healthcare provider.

The money can be used to pay for medical expenses, household bills, transportation, childcare, lost income, or any other financial needs during recovery.

How Hospital Indemnity Insurance Works

After purchasing a hospital indemnity insurance policy and paying the required premiums, you become eligible for cash benefits if you experience a covered hospitalization. Depending on your policy, benefits may be paid for hospital admission, each day spent in the hospital, intensive care unit (ICU) stays, surgeries, or other covered medical events.

The benefit amount is predetermined and does not depend on the actual hospital bill. Once your claim is approved, the insurance company sends the payment directly to you.

Why Hospital Indemnity Insurance is Important

Even with comprehensive health insurance, many people still face significant out-of-pocket medical costs. Deductibles, copayments, coinsurance, non-covered services, travel expenses, and lost wages can create financial stress during hospitalization.

Hospital indemnity insurance provides additional financial support by offering cash benefits that help cover these unexpected costs without restrictions on how the money is spent.

What Does Hospital Indemnity Insurance Cover?

Coverage varies by insurance company and policy, but many plans include benefits for:

- Hospital admission

- Daily hospital confinement

- Intensive Care Unit (ICU) stays

- Emergency hospitalization

- Surgical procedures

- Observation stays

- Outpatient surgery

- Rehabilitation services

- Recovery care

- Ambulance transportation

- Accidental injuries

- Critical illnesses (if included in the policy)

Always review the policy details to understand covered services and exclusions.

Expenses You Can Pay With Hospital Indemnity Benefits

One of the biggest advantages of hospital indemnity insurance is flexibility. Cash benefits can be used for:

- Health insurance deductibles

- Copayments

- Coinsurance

- Prescription medications

- Transportation expenses

- Hotel accommodations for family members

- Childcare costs

- Utility bills

- Mortgage or rent payments

- Grocery expenses

- Lost income during recovery

- Any other personal financial needs

There are generally no restrictions on how the benefit payment is used.

Who Should Consider Hospital Indemnity Insurance?

Hospital indemnity insurance may be a good option for:

- Individuals with high-deductible health plans

- Families seeking additional financial protection

- Self-employed workers

- Small business owners

- Retirees

- Medicare beneficiaries

- People with limited emergency savings

- Individuals with physically demanding jobs

- Employees whose workplace offers supplemental insurance benefits

Hospital Indemnity Insurance vs Health Insurance

Although both types of insurance help during medical events, they serve different purposes.

Traditional health insurance pays healthcare providers for covered medical services, while hospital indemnity insurance pays fixed cash benefits directly to the policyholder after a covered hospitalization.

Hospital indemnity insurance is not intended to replace comprehensive health insurance. Instead, it supplements existing medical coverage by helping with out-of-pocket expenses.

Common Hospital Indemnity Insurance Benefits

Hospital Admission Benefit

Many policies provide a one-time payment when you are admitted to the hospital for a covered reason.

Daily Hospital Benefit

You may receive a fixed cash amount for each day you remain hospitalized, subject to policy limits.

Intensive Care Unit Benefit

Additional daily payments are often available if treatment requires admission to an intensive care unit.

Surgical Benefit

Some policies include cash benefits for qualifying inpatient surgical procedures.

Observation Benefit

Certain plans provide benefits for observation stays that do not result in full hospital admission.

Advantages of Hospital Indemnity Insurance

Hospital indemnity insurance offers several valuable benefits:

- Helps cover unexpected hospital expenses

- Provides direct cash payments

- Can be used for both medical and non-medical costs

- Supplements existing health insurance

- Reduces financial stress during recovery

- Offers predictable benefit amounts

- Provides additional protection for high-deductible health plans

Limitations of Hospital Indemnity Insurance

Although beneficial, hospital indemnity insurance also has limitations.

Benefits are fixed and may not fully cover expensive hospital bills. Policies often include waiting periods, benefit limits, exclusions, and eligibility requirements. Some plans only cover hospitalizations resulting from specific illnesses or accidents.

Carefully reviewing policy documents before purchasing is essential.

Factors to Consider Before Buying

When comparing hospital indemnity insurance policies, evaluate:

- Monthly premium

- Hospital admission benefit amount

- Daily hospitalization benefit

- ICU coverage

- Waiting periods

- Maximum benefit limits

- Covered illnesses and injuries

- Exclusions

- Claim process

- Insurance company reputation

- Renewal terms

Comparing multiple policies helps ensure you choose the best value.

Best Hospital Indemnity Insurance Providers

Several well-known insurance companies offer hospital indemnity insurance products, including:

- Aflac

- Cigna Healthcare

- Mutual of Omaha

- Colonial Life

- ManhattanLife

- Humana

- UnitedHealthcare

- Allstate Benefits

Available plans, benefit amounts, and eligibility requirements vary by provider and state.

How Much Does Hospital Indemnity Insurance Cost?

The cost depends on several factors, including:

- Age

- State of residence

- Coverage level

- Benefit amounts

- Health status

- Insurance company

- Optional riders

Many basic policies are relatively affordable, making hospital indemnity insurance accessible for individuals seeking additional financial protection.

How to File a Claim

Most insurance companies require:

- Completed claim form

- Hospital admission records

- Discharge summary

- Physician documentation

- Itemized hospital bill (if requested)

- Proof of covered hospitalization

Many insurers now offer online claims submission, making the process faster and more convenient.

Frequently Asked Questions

Is hospital indemnity insurance worth it?

It can be valuable for individuals with high deductibles, limited savings, or concerns about unexpected hospitalization expenses. It provides additional financial support that traditional health insurance may not cover.

Does hospital indemnity insurance replace health insurance?

No. Hospital indemnity insurance is supplemental coverage and should not replace comprehensive health insurance.

Can I use the cash benefit for non-medical expenses?

Yes. Most policies allow you to use benefit payments for any purpose, including rent, groceries, transportation, childcare, or household bills.

Does Medicare cover all hospital expenses?

No. Medicare beneficiaries may still have deductibles, coinsurance, and other out-of-pocket costs. Hospital indemnity insurance can help offset these expenses.

Can I have more than one hospital indemnity insurance policy?

In many cases, yes. Some individuals purchase multiple supplemental policies, although eligibility and benefits depend on each insurer’s terms and conditions.

Conclusion

Hospital indemnity insurance provides an additional layer of financial security by paying cash benefits directly to policyholders during covered hospital stays. While it does not replace traditional health insurance, it helps reduce the impact of deductibles, copayments, lost income, and other unexpected expenses that often accompany hospitalization. Before purchasing a policy, compare benefit amounts, premiums, exclusions, waiting periods, and claim procedures from multiple insurers. Choosing the right hospital indemnity insurance plan can provide peace of mind and valuable financial support when you need it most.

Related posts:

Best Hospitals in the USA 2025: A Complete Guide to America’s Top Medical Institutions

Best Hospitals in the USA 2025: A Complete Guide to America’s Top Medical Institutions

Best Organ Transplant Hospitals in the USA (2025): Where Life Gets a Second Chance

Best Organ Transplant Hospitals in the USA (2025): Where Life Gets a Second Chance

Best Hospital in Germany

Best Hospital in Germany

Health Insurance for Hospital Bills: A Complete Guide

Health Insurance for Hospital Bills: A Complete Guide

Fertility Hospital Near Me: Complete Guide to Choosing the Best IVF & Fertility Clinics

Fertility Hospital Near Me: Complete Guide to Choosing the Best IVF & Fertility Clinics

Best Private Hospital in Los Angeles: A Complete Guide

Best Private Hospital in Los Angeles: A Complete Guide

Cardiac Bypass Surgery in International Hospitals: Cost, Best Countries, and Patient Guide

Cardiac Bypass Surgery in International Hospitals: Cost, Best Countries, and Patient Guide

Best Hospital in Malaysia: Top International Healthcare Guide

Best Hospital in Malaysia: Top International Healthcare Guide

Top Fertility Clinics in America: Leading Centers for Advanced Reproductive Care

Top Fertility Clinics in America: Leading Centers for Advanced Reproductive Care

Best IVF Hospital in USA: Leading Centers for Advanced Fertility Treatment

Best IVF Hospital in USA: Leading Centers for Advanced Fertility Treatment