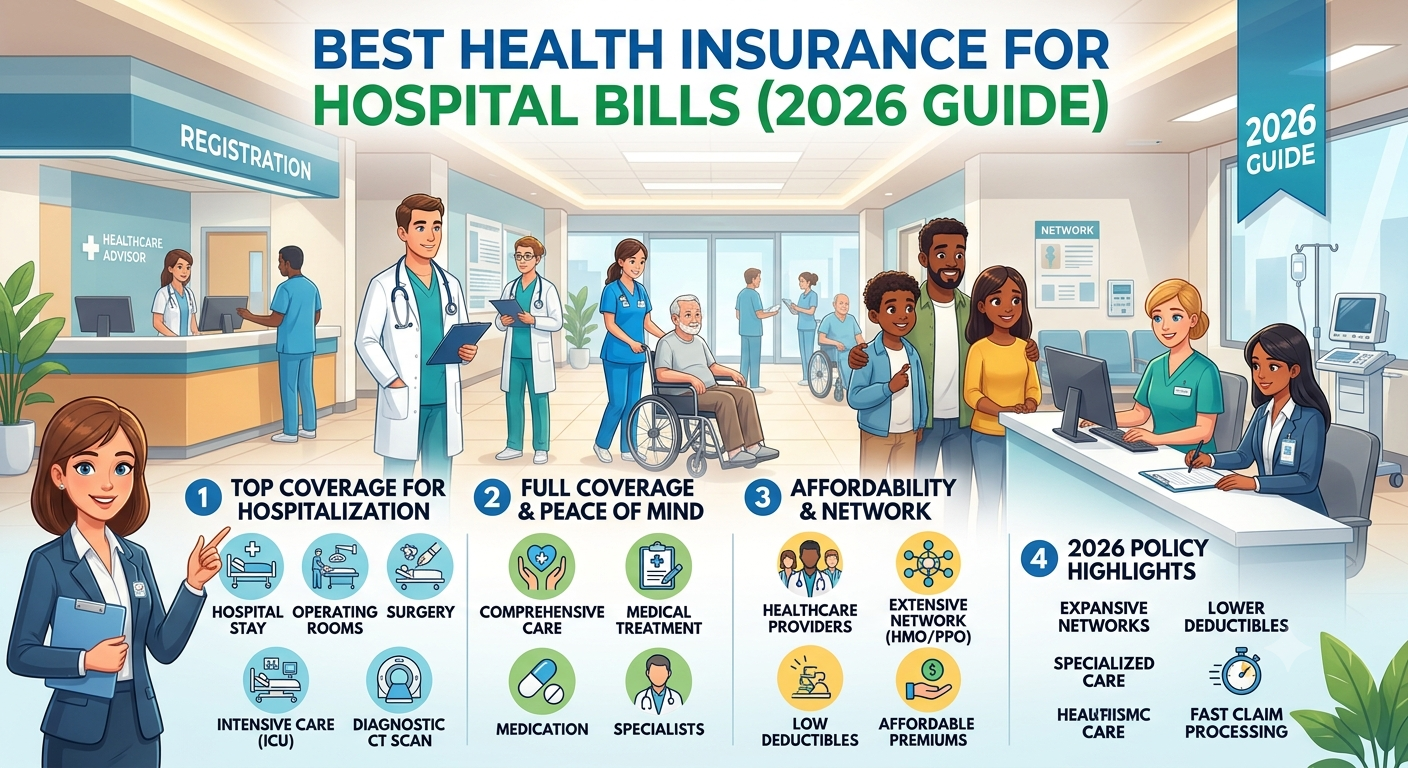

Medical expenses continue to rise every year, making health insurance one of the most important financial investments for individuals and families. A single hospitalization can cost thousands of dollars, and without proper insurance coverage, these expenses can quickly become a financial burden. Whether it is an emergency surgery, treatment for a chronic illness, or a planned medical procedure, the right health insurance plan can protect your savings while ensuring access to quality healthcare.

Choosing the best health insurance for hospital bills requires understanding coverage options, premiums, deductibles, provider networks, and additional benefits. Every insurance plan is different, and selecting the right one depends on your healthcare needs, budget, and lifestyle.

This comprehensive guide explains how health insurance works, the best types of plans for hospital expenses, important features to compare, and practical tips for selecting the right policy.

Why Health Insurance is Important

Health insurance is designed to reduce the financial impact of medical emergencies. Instead of paying the full cost of hospital treatment, insured individuals pay only a portion of the expense, depending on their policy.

The main benefits include:

- Lower hospitalization costs

- Access to quality healthcare providers

- Emergency medical coverage

- Financial protection against unexpected illnesses

- Preventive healthcare benefits

- Coverage for surgeries and specialist treatments

- Prescription drug assistance

- Peace of mind during medical emergencies

Without insurance, even a short hospital stay can result in significant medical debt.

What Does Health Insurance Cover?

Most comprehensive health insurance plans provide coverage for:

Inpatient Hospitalization

This includes expenses such as:

- Room charges

- ICU charges

- Nursing services

- Surgical procedures

- Physician fees

- Medical equipment

- Diagnostic tests

- Medicines administered during hospitalization

Emergency Room Visits

Emergency treatment following accidents, injuries, heart attacks, or sudden illnesses is usually covered.

Surgery Costs

Insurance generally covers:

- General surgery

- Cardiac surgery

- Orthopedic surgery

- Cancer surgery

- Organ transplant procedures (subject to policy terms)

Diagnostic Tests

Hospital bills often include:

- MRI

- CT Scan

- Blood tests

- X-rays

- Ultrasound

- ECG

- Laboratory investigations

Many insurance plans cover these costs.

Prescription Medicines

Hospital-administered medications and, in many plans, post-discharge prescriptions are also covered.

Ambulance Services

Emergency ambulance transportation is included in many modern health insurance policies.

Types of Health Insurance Plans

Individual Health Insurance

Designed for one person.

Best for:

- Young professionals

- Students

- Self-employed individuals

Advantages include customized coverage and individual deductibles.

Family Health Insurance

One policy covers the entire family.

Suitable for:

- Married couples

- Parents

- Children

It is often more affordable than buying separate policies.

Employer-Sponsored Insurance

Many companies provide health insurance as part of employee benefits.

Advantages include:

- Lower premiums

- Employer contribution

- Large provider networks

Senior Health Insurance

Specially designed for people over 60 years of age.

Usually includes:

- Higher hospitalization coverage

- Chronic disease management

- Specialized treatments

Critical Illness Insurance

Provides a lump-sum payment upon diagnosis of serious illnesses such as:

- Cancer

- Stroke

- Heart attack

- Kidney failure

It supplements standard health insurance.

Features to Look for in the Best Health Insurance

Comprehensive Hospital Coverage

The policy should cover:

- Hospital room

- ICU

- Surgery

- Medicines

- Medical procedures

- Specialist consultations

Avoid plans with excessive exclusions.

Cashless Hospital Network

Cashless treatment allows hospitals to directly settle bills with the insurance company.

Benefits include:

- No large upfront payments

- Faster admission process

- Less paperwork

Affordable Premium

A lower premium is attractive but should not come at the expense of inadequate coverage.

Balance affordability with benefits.

Low Deductible

The deductible is the amount you pay before insurance starts covering expenses.

Lower deductibles reduce your out-of-pocket costs during hospitalization.

High Coverage Limit

Hospital costs continue to increase every year.

A higher coverage limit provides better financial security.

No Claim Bonus

Many insurers reward policyholders with increased coverage or discounted premiums if no claims are made during the policy year.

Pre and Post Hospitalization

Look for plans covering:

- Doctor consultations

- Diagnostic tests

- Medicines before admission

- Follow-up treatment after discharge

Daycare Procedures

Modern treatments often require less than 24-hour hospitalization.

Good insurance plans cover daycare procedures such as:

- Cataract surgery

- Dialysis

- Chemotherapy

- Endoscopy

Common Hospital Expenses Covered

Hospital bills usually include:

- Admission charges

- Room rent

- ICU charges

- Doctor fees

- Specialist consultation

- Surgery

- Medical supplies

- Laboratory tests

- Imaging services

- Pharmacy charges

- Nursing services

- Oxygen support

- Emergency treatment

- Medical devices

- Discharge medicines

A quality health insurance plan should cover most of these expenses.

Factors Affecting Health Insurance Premiums

Premiums depend on several factors.

Age

Older individuals generally pay higher premiums due to increased health risks.

Medical History

Pre-existing medical conditions often increase insurance costs.

Lifestyle

Smoking, obesity, and certain lifestyle habits can affect premiums.

Location

Healthcare costs differ by region, influencing insurance pricing.

Coverage Amount

Higher coverage limits usually result in higher premiums.

Deductible

Higher deductibles often lower monthly premiums.

Best Health Insurance Companies

Several well-known insurers offer comprehensive hospital coverage.

Popular providers include:

- UnitedHealthcare

- Blue Cross Blue Shield

- Kaiser Permanente

- Aetna

- Cigna

- Humana

- Molina Healthcare

- Oscar Health

Each company offers different plans with varying premiums, provider networks, and benefits. Comparing multiple options helps you find the best fit for your healthcare needs.

How to Choose the Best Health Insurance

Compare Multiple Plans

Never buy the first plan you see.

Compare:

- Premiums

- Deductibles

- Hospital network

- Claim settlement process

- Annual coverage

- Prescription benefits

Check Network Hospitals

Ensure your preferred hospitals are included in the insurer’s provider network.

This reduces treatment costs significantly.

Read Policy Exclusions

Understand what is not covered.

Common exclusions may include:

- Cosmetic surgery

- Experimental treatments

- Certain pre-existing conditions during waiting periods

- Non-medical expenses

Understand Waiting Periods

Some treatments become eligible only after a waiting period.

Always review these conditions before purchasing.

Review Claim Process

A simple and fast claims process reduces stress during emergencies.

Look for insurers with digital claims and 24/7 customer support.

Tips to Reduce Hospital Bills

Even with insurance, smart healthcare decisions can reduce costs.

Choose In-Network Hospitals

Insurance companies negotiate discounted rates with network hospitals.

Use Preventive Care

Regular health checkups help detect illnesses early and reduce hospitalization risk.

Understand Your Policy

Know:

- Coverage limits

- Co-payments

- Deductibles

- Exclusions

Keep Medical Records

Maintain copies of:

- Prescriptions

- Diagnostic reports

- Hospital bills

- Discharge summaries

These documents simplify claim approval.

Buy Insurance Early

Purchasing insurance while young generally offers:

- Lower premiums

- Better coverage

- Shorter waiting periods for future claims

Common Mistakes When Buying Health Insurance

Many buyers make avoidable mistakes.

These include:

- Choosing the cheapest policy without comparing benefits

- Ignoring policy exclusions

- Selecting insufficient coverage

- Not checking hospital networks

- Overlooking deductibles and co-payments

- Hiding medical history during application

- Failing to renew the policy on time

Avoiding these mistakes can save substantial money during hospitalization.

Frequently Asked Questions

Which health insurance is best for hospital bills?

The best health insurance plan is one that offers comprehensive hospitalization coverage, a wide hospital network, affordable premiums, cashless treatment, and strong customer support.

Does health insurance cover surgery?

Most comprehensive health insurance plans cover medically necessary surgeries, including surgeon fees, anesthesia, operating room charges, and hospitalization costs.

Are emergency hospital visits covered?

Yes. Most health insurance policies cover emergency room visits and emergency hospitalization, subject to policy terms and conditions.

Is cashless hospitalization better?

Yes. Cashless hospitalization allows the insurer to settle eligible hospital bills directly with the hospital, minimizing out-of-pocket expenses.

How much health insurance coverage is enough?

The ideal coverage amount depends on factors such as age, family size, medical history, and local healthcare costs. Higher coverage limits generally provide better protection against expensive hospital treatments.

Conclusion

Health insurance is one of the most effective ways to protect yourself and your family from the financial impact of unexpected hospital bills. A well-chosen policy can cover hospitalization, surgeries, emergency care, diagnostic tests, prescription medicines, and many other healthcare expenses while providing access to quality medical facilities.

Before purchasing a plan, compare coverage options, premiums, deductibles, hospital networks, exclusions, and claim processes. Selecting comprehensive health insurance today can help safeguard your finances and ensure timely medical care when you need it most.

With rising healthcare costs worldwide, investing in the right health insurance policy is not just a financial decision—it is an essential step toward long-term health and financial security.

Related posts:

Best Hospitals in the USA 2025: A Complete Guide to America’s Top Medical Institutions

Best Hospitals in the USA 2025: A Complete Guide to America’s Top Medical Institutions

Best Organ Transplant Hospitals in the USA (2025): Where Life Gets a Second Chance

Best Organ Transplant Hospitals in the USA (2025): Where Life Gets a Second Chance

Top 10 Best Hospitals in Canada

Top 10 Best Hospitals in Canada

Top 10 Best Hospitals in Europe

Top 10 Best Hospitals in Europe

Hospital Alcohol Detox: A Comprehensive Guide to Safe Recovery

Hospital Alcohol Detox: A Comprehensive Guide to Safe Recovery

Dermatological Problems: Causes, Symptoms, and Treatment Options

Dermatological Problems: Causes, Symptoms, and Treatment Options

Mayo Clinic USA: A Global Leader in Healthcare

Mayo Clinic USA: A Global Leader in Healthcare

Best Hospital in Malaysia: Top International Healthcare Guide

Best Hospital in Malaysia: Top International Healthcare Guide

Top Rated Hospitals in America: A Comprehensive Guide to World Class Healthcare

Top Rated Hospitals in America: A Comprehensive Guide to World Class Healthcare

Medical Insurance USA: Complete Guide to Choosing the Best Health Coverage in 2026

Medical Insurance USA: Complete Guide to Choosing the Best Health Coverage in 2026